Our Help Section: Your reliable partner for important questions and solutions in Reental

How orIt works with all with innovative and disruptive technologies, some public entities take a long time to adapt to these new trends, a fact that occurs mainly in public institutions because they are bureaucratic “giants”. The State often lags behind new trends in technology for months or even years when it comes to establishing legal bases or accommodating them in aspects such as tax reporting.

Las Cryptocurrencies are one of the most talked about topics in recent years, due to their great economic implications, their use in various projects and even their use as a means of payment in different countries.

And as expected, governments have taken several years to adapt or create laws that protect investors in these digital assets, so that until now these investors have been in a kind of lawless limbo.

As hard and tedious as it sounds It is necessary for us to declare the income derived from the activity with cryptocurrencies, both abroad and in the country of origin.

In this article we are going to make a brief review of the main aspects to consider when declaring these assets, such as the activities that can be carried out with cryptocurrencies, which of these must be declared, in which taxes we must charge our profits and finally a tutorial on how to declare cryptocurrency earnings in the income tax return.

Cryptocurrency activity and which of them should I declare

First of all, we must make it clear that the payment of taxes will depend on the use we make of our cryptocurrencies, that is, depending on what we do with those cryptocurrencies, we must pay some taxes or others.

In Spain, the main taxes that must be paid are Personal Income Tax (IRPF), Value Added Tax (VAT) and Wealth Tax (IP). Although it should be noted that there are also other taxes such as the Economic Activities Tax (IAE) or the Inheritance and Gift Tax (ISD).

Now let's see which of these taxes we should pay depending on the activity we do and which we would be exempt from.

VAT

First, we must bear in mind that Bitcoin and other cryptocurrencies are considered a means of payment in the European Union, so the purchase and sale of these assets is not affected by Value Added Tax. If you only invest in cryptocurrencies, that is, buying and selling these assets, you should not worry about VAT.

On the other hand, you should consider that if you use cryptocurrency to pay for a product or service, just as you would with euros or dollars, this activity is affected by VAT, since that good or service carries the corresponding VAT (normally 21%) regardless of the way in which you pay it.

PERSONAL INCOME TAX

First of all, note that this tax taxes the income earned during the calendar year of a natural person resident in Spain and that it is regulated by means of the income tax return.

Cryptocurrency buying and selling

Most investors decide to invest in cryptocurrencies to obtain a return and thus multiply their invested capital, and although this usual practice is exempt from VAT, it is not exempt from personal income tax. Therefore, those profits derived from the acquisition and transfer or sale of cryptocurrencies must be declared in personal income tax, specifically in the area of capital gains and losses. In other words, if we had bought 1 Bitcoin at a price of €10,000 and after a year it had doubled its price (€20,000), we should declare our profit (€10,000) as follows.

For the first 6,000 euros of profits we would pay the 19% tax, that is, 1,140 euros, while for the 4,000 euros we have left until 10,000 euros we would pay 21%, that is, 840€. So finally, for our profits of €10,000, we should pay a total of €1,980 in Personal Income Tax.

Increase in the price of my cryptocurrencies

And what happens if the price of my cryptocurrency has multiplied x2 but I haven't sold it? In this case, we should not tax those profits because we have not obtained liquid profits by not selling. If you don't sell your cryptocurrencies, you should not tax their rise.

Exchange between different cryptocurrencies

In the case of exchanging between different cryptocurrencies, we would also be required to pay taxes according to the Tax Agency. Even if we do not transfer our cryptocurrencies to euros, we must declare if, at the time of the exchange with any cryptocurrency, if we have made a profit due to the increase in the price of our crypto (the 10,000€ of profit in the previous example), we should tax this income in personal income tax.

Profits and losses in cryptocurrency

Let's put another scenario, what happens if I have earned money buying and selling some cryptocurrencies, but in other cryptocurrencies I have had losses? This scenario is integrated into what is known as the savings tax base, and would be added to the rest of the capital gains and losses. This is where the concept of compensation for capital gains and losses comes into play, which implies that we must only pay taxes on the real income received from our activities. In other words, we will only have to declare the income minus the losses we have had, which is known as real profit.

Wealth Tax

This tax integrates everything you own, taxes the assets of individuals and is calculated based on the value of all our assets as of December 31. Some autonomous communities have an exempt minimum so that only people with large assets must tax their IP, in general this minimum is set at 700,000 euros of assets.

Then we must know that in the sum of all our assets that make up our assets we must add our cryptocurrencies, depending on their price as of December 31, and add it to the rest of our assets such as stocks, real estate, current accounts or land.

Model 720

This model is the informative declaration on assets and rights located abroad, this declaration must be submitted from March 1 to 31 if the value we have abroad of our accounts, securities or real estate exceeds €50,000 as of December 31. Therefore, if we have our cryptocurrencies in an Exchange outside of Spain and we exceed the mentioned amount of €50,000, we must present this model, on the other hand, if we have our cryptocurrencies in a cold wallet such as Ledger or Trezor, they are considered to be in Spain, so we should not present this model.

How to declare

Finally, let's see the reason why we're here, we're going to present you with a step by step to declare our different cryptocurrency earnings in the income tax return.

It is already at the first point where people start to have problems, because collecting a large number of the transactions in which we have generated income, in addition to different exchanges, can be a very heavy task.

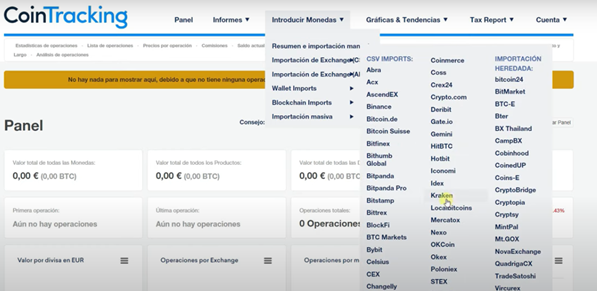

Everyone can track their cryptocurrency transactions in any way they want, at Reental we consider using the Coin Tracking program, since it is a faster and easier way to collect all our transactions to be presented on the income tax return. You can create an account in just 2 minutes and enjoy this platform.

This platform allows us to upload the csv file that we download from the different Exchanges that contain our operations, and then the platform collects all the files for us to have an overview of all our operations. Regarding Coin Tracking, it should be noted that its free plan has a maximum of 200 operations and a maximum csv file size of 5 MB, however, we consider that these numbers are quite correct for the common investor, so with the free version you can rest assured.

If you have any questions about downloading and importing the csv files, Coin Tracking itself explains how to do it on each of the Exchanges.

Once the file has been imported, the program will show us all the operations performed on that Exchange.

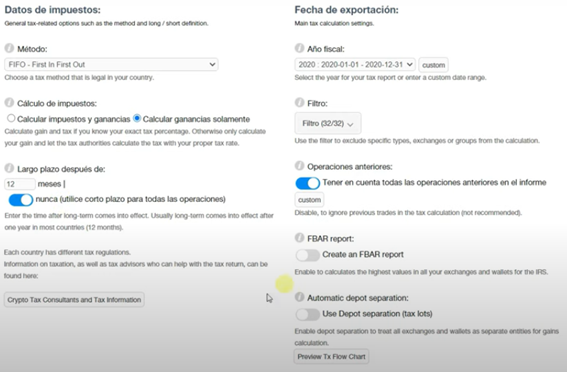

All right, once we have our Coin Tracking account and our operations in order, it's time to obtain our tax report to be able to declare our cryptocurrency earnings on our income tax return.

To obtain our tax report we must click on the Tax Report tab in the main menu.

Once there from Reental, we recommend leaving all the fields to be filled in as follows:

Once all the fields are filled in, we will click on this button to create our report. At this point we would already have our report created in which we could see the capital gains obtained from the sale of our cryptocurrencies, as well as the different income obtained from airdrops, staking, lending our cryptocurrencies or mining.

The next step would be to go directly to our draft income tax return, in which we must click on the sections tab:

Below we present the different activities that have been able to generate income from the use of cryptocurrencies, in which sections and subsections must be taxed and how taxation is carried out. All the required data can be found in the Coin Tracking tax report:

Staking or interest for having lent our cryptocurrencies to third parties:

Fill the entire performance with data but without retention.

Buying and selling or swapping between cryptocurrencies:

Airdrops or referral programs:

Once all the steps we have discussed in the different activities have been completed, we would have finalized our income tax return on our income derived from cryptocurrencies.

If you still have any questions about this process, you can contact a tax advisor to facilitate the process and prevent you from forgetting any aspect to declare.

By the way! Don't forget to take a look at the articles in our blog. Welcome to the Reental community.