One of the big decisions we face when we start working and we have some liquidity is to decide if I am dealing with a savings strategy or if, on the contrary, I am doing it towards investment.

To shed light on these two commonly mixed terms, I will use the example of the primary productive sector. A farmer produces in order to recover his investment during the growing season: water, diesel, seeds, fertilizer products, amortization of machinery, etc... But also to generate a surplus. Formerly, it was produced for self-sufficiency, that is, to consume what you generated yourself. And if you were able to generate more, you stored it and even took it to the market to exchange it for another product you needed. Here we link concepts such as need, production, exchange.

In net production terms, if you produced more than necessary, you would be saving. Let's imagine that you grow potatoes, and you manage to have a 50% surplus. Given the short-lived nature of potatoes, you could only enjoy your surplus for a limited time, meaning your savings would tend to be lost.

It was an unsafe and unusable savings. Therefore, the use of markets, to be able to come with your surplus and to be able to exchange it for something that would meet our current need or another future need. It would be the case, therefore, of buying seeds.

Now, let's imagine that we decided to buy 20% more seeds than compared to last year, or for example, that we decided to buy 20% more seeds from another species. We could say that it is a future investment, given that we would be expecting to increase production by approximately 20%. The nuance is subtle, I always have to buy seeds, but buying a little more would no longer be saving, it would be investing. That's why we mix the terms so often, because space time is what qualifies.

For all these reasons, savings are a concept rooted in future security, to maintaining its value in the future and to having it available quickly, to deal with an unexpected event or an exceptional situation. However, the concept of investment is rooted in a closer future value but of greater value, that is, of capital gain. And therefore, it involves a risk of success.

However, at present, the concept of risk is not at all clear. I mean, who guarantees me that today 10,000 euros will be worth 10 years from now, those same 10,000 euros. You don't have to answer: no one. Because they won't be worth it.

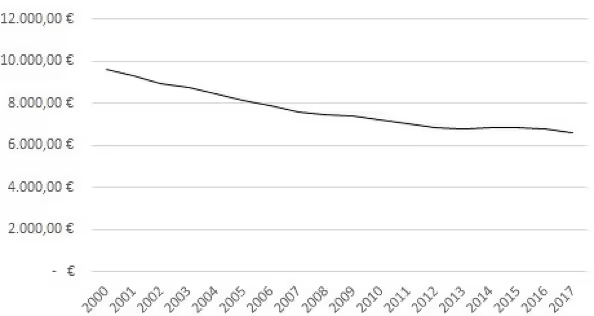

As you can see in the previous graph, the loss in value in 7 years has been approximately 40%, and probably close to 50% in 10 years. We will have to wait until 2021, to see the real impact that Covid has had on our economy.

That's why the term savings no longer makes sense. Because we are looking for security and even more: guarantee and reserve of value. So we should use the term investment. We understand that there is risk, but let's understand that if we just leave the money in an account, it will be worth half of it over time and with a similar risk.

This should be on everyone's lips, however, no one directly verbalizes this type of forecast. They only mention inflation or GDP in isolation, yet they don't talk about the impact that this loss of purchasing power has on citizens.

Once a person begins to save money, they begin to lose purchasing power as a result of the inflationary system that all countries are governed by. When we talk about purchasing power, we talk about the economic power of money. The goal is not to have 10,000 euros and keep it for 10 years, the objective is to have 10,000 euros and that over the years, with that same amount you can continue to buy, at least, as much as in the beginning.

As we can see in the previous graph, inflation has been constant over the years and has been causing the savings of all citizens to lose purchasing power as it has been generated, that is, every year they are worth less. Murray R. Rothbard says in his book”What has the government done to our money?”

“If the government finds a way to counterfeit money by creating it out of thin air, it could make money without bothering to sell its products or extract gold. In this way, it cleverly appropriates resources in a subtle way, without causing the hostility that taxes raise”

It is important to be clear about what causes inflation and that it has nothing to do with established taxes such as personal income tax, VAT, IS, IE, etc. If we compare the impact of inflation on savings, with the impact that taxes have on our profits, we will see that with the average inflation of the last 20 years, the comparison would be useless, assuming that for a saver, the money that disappears because of inflation is light years away from the one that disappears because of established taxes.

In a more complete definition, we can define inflation as the increase in the price we pay for goods and services, but it is also the increase in money supply in the system. This act represents a hidden tax for consumers and is the main cause of inflation. The period in which money support increases, the currency weakens and the prices of goods rise, this process takes between 18 months and 2 years.

Perhaps now, after understanding this phenomenon, we will not see in such a positive way the news that comes out about injecting liquidity into markets through printing and creating money by central banks.

It's time to act and to start moving your savings, your liquidity and your head. It seeks profitability and liquidity.