I have crypto assets and... What now?

In this post, I want to reflect on the usability of crypto assets beyond the mere fact of owning them.

We are living in a time of passion and buying cryptoassets, even without a deep understanding of what they are about, without knowing the details of the functionalities of the project whose token you are purchasing, or without seeking to know the founding team (very bad for anyone who works like that, by the way).

You will always hear us that the first thing before starting to invest simply to follow the trends is to study, read and have a judgment on your investments, understanding the risks and profits associated with that investment.

With that said, I would like to launch a reflection on how to use the tokens you acquire, as if they were digital assets. This would be equivalent to when we buy a property, a vehicle for work, or any machinery that generates performance. In this way, your assets can not only give you returns because of their own increase in value over time, but they can produce for extra value.

Well, we are at a very interesting time when the opportunity opens up to being able to deposit these digital assets, as collateral or collateral, for the loan application. It would be a service similar to the one provided by a mortgage, where they lend you an economic amount (in our case in crypto currency) equivalent to a percentage of the value of that asset.

This offers us the way to avoid having to go out into the Fiat world and lose our exposure to a certain asset (Bitcoin, Ether, Dot, etc.) to either obtain timely liquidity or, and this is the purpose of this post, to use that debt to invest in another project whose return exceeds the value of the interest on the loan plus a percentage of extra return. Through this use, these products allow for a more efficient use of your crypto capital.

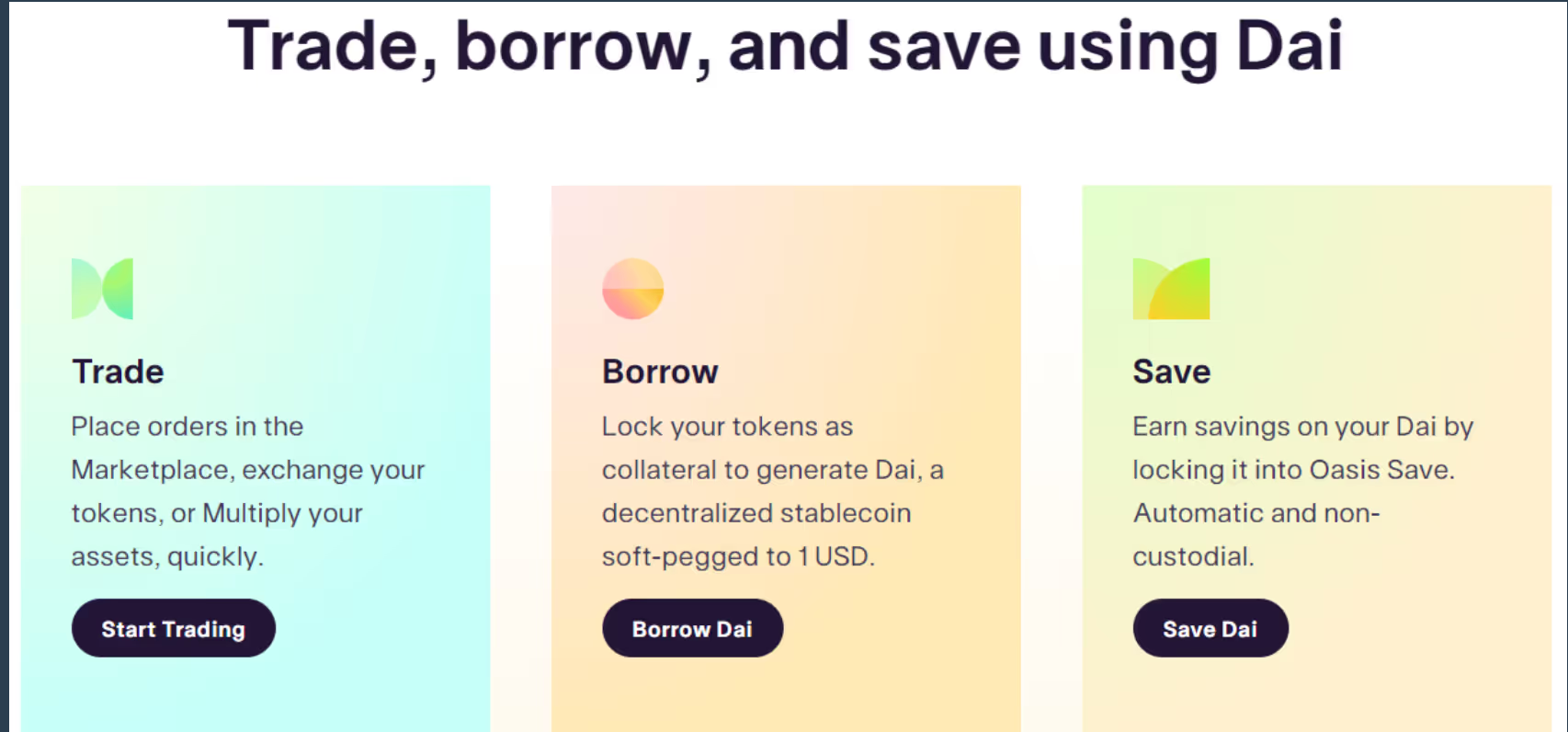

The first decentralized project to appear on Collateralized Debt Positions (CDP), in Spanish “Collateralized Debt Position or Obligation”, was Maker Dao (late 2017). And it started with the collateralization of ETH to obtain Dai.

In this image we see the Oasis platform, from Maker DAO.

Later, other projects were added, such as Aave on Ethereum or Venus in the BSC, and Crypto, Nexo and Celsius came out in CeFi (Centralized) format. Its CDP offer ranges from a maximum collateralization of 30 to 70%, depending on the characteristics of the active crypto.

However, we must properly calculate the risk of this operation, given that crypto projects tend to follow the bullish-bearish market pattern (led by Bitcoin). In other words, if the value of our collateral falls, our loan will tend to exceed the degree of collateralization and could be liquidated (in an extreme case). To reduce this overexposure to the market, given that we have our collateralized capital and our loan, we could choose a project that does not follow the market pattern, in order to diversify in a more efficient way.

Remember that the objective of applying for the loan is to obtain a return greater than the interest rate, but above all not to lose value with respect to the market. If that situation were to arrive, we would have to deal with the loan, surely liquidating part of the collateral.

And at this point, it's very interesting to have projects that have their base built on a traditional asset: real estate, debt, future cash flows, etc. And that therefore have two characteristics:

1) not following the trend of the crypto market, and

2) have a less volatile return but higher than the interest rate of the loan.

If we were to make a practical example it would be something like this:

I deposit 100 monetary units and collateralize them on a platform (DeFi or CeFi), I obtain a 50% loan for those assets, that is, 50 monetary units.

If the interest rate is 5%, I need to obtain a higher return to do an interesting business, and if the crypto market is giving 20%, that would be our goal.

If we invest those 50 units in a real estate asset tokenization project, we get 12%. Value that is below the market, but nevertheless, is giving us 7 points above the cost of the loan.

Once the loan is finalized and repaid, we would be obtaining an extra return of 3.5 monetary units.

In addition, the value of the collateral may increase in value, as in the case of bitcoin, ether or others. So you can also self-pay the loan with this increase in value.

The Reental project or similar fits into these investment models or strategies, since it reduces volatility, risks and focuses on stronger returns.

We always recommend that you inform yourself well, understand the risks and even have the help of a qualified advisor to analyze your profile and expectations.

More information at our website.